U.S. & Canada Digital Water Market To Surge 107% By 2033 As Utilities Accelerate Their Own Transformations

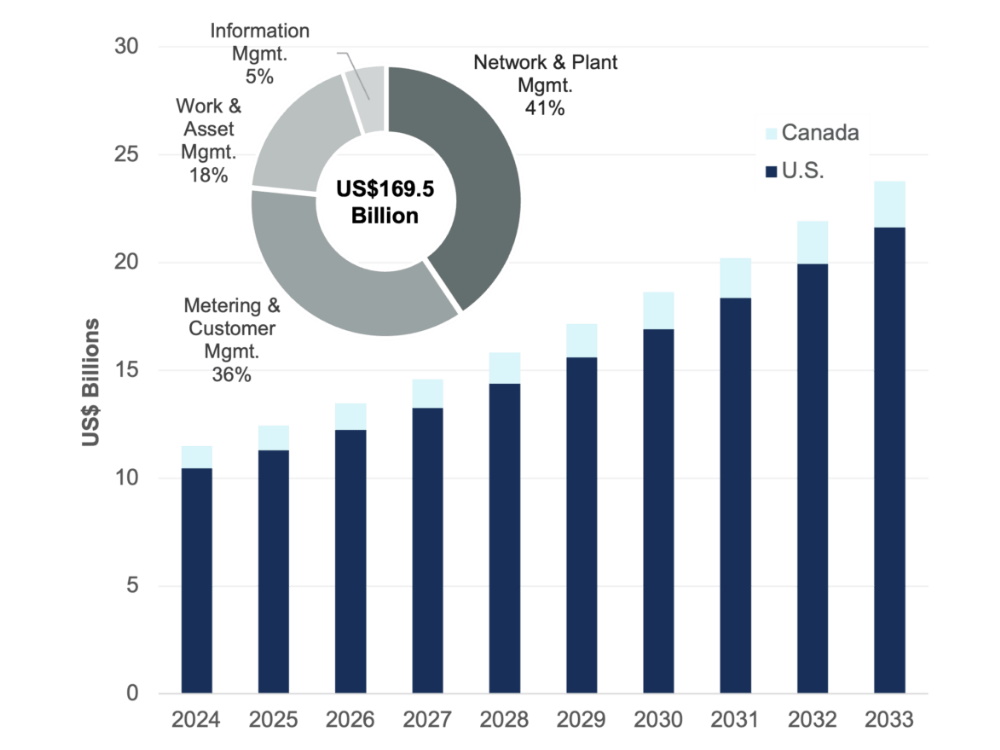

Water utilities of all sizes are increasingly adopting digital water solutions to tackle myriad of challenges, from regulatory shifts and retiring workforces to aging infrastructure and climate risks. A new report from Bluefield Research forecasts strong demand for digital water solutions in the U.S. and Canada, with the market projected to grow from US$11.5B in 2024 to US$23.8B by 2033.

“The adoption of digital solutions is not just inevitable—it is critical for utilities to ensure the resilience and sustainability of water systems,” says Christine Ow, Digital Water Analyst at Bluefield Research. “Companies are transforming their digital water offerings to provide increasingly accessible solutions for utilities, even to resource-strapped small and mid-sized water utilities in the U.S. and Canada.”

With cumulative digital water spend expected to total US$169.5B from 2024 to 2033, this expansion—driven by an 8.4% compound annual growth rate (CAGR)—highlights the growing reliance on digital technologies (e.g., smart meters, network monitors, and data management) to manage utility assets more efficiently.

Exhibit: U.S. & Canada Digital Water Market Outlook, 2024–2033

One of the most urgent challenges facing the water sector is the rapidly retiring workforce. From 2015 to 2023, the utility workforce vacancy rate in the U.S. & Canada has doubled, according to the U.S. Department of Labor and Statistics Canada. With experienced professionals retiring, utilities must find ways to transfer their knowledge and expertise. “The emergence of artificial intelligence (AI) and machine learning (ML) will not only be crucial in bridging the widening workforce gap, these technologies will also reshape utility operations through optimized data analytics, predictive maintenance, and streamlined operations,” says Ow.

Tightening regulations on water quality, leakage management, and water supplies are further pushing water utilities toward digital solutions. Real-time data collection and management technologies are becoming essential to ensure compliance, boost operational efficiency, and improve resource management. Federal initiatives, such as the U.S. Infrastructure Investment and Jobs Act (IIJA) and Canada’s Investing in Canada Infrastructure Plan, are accelerating this shift by providing critical funding for key water industry projects.

“Traditional digital water solutions—such as SCADA (Supervisory Control and Data Acquisition), GIS (Geographic Information Systems), and metering—still account for over 75% of the forecasted growth in total spend. However, that’s only part of the story,” says Ow, highlighting the growing impact of newer technologies reshaping the future of water management.

Cloud-based platform solutions will experience rapid double-digit growth in the water sector, driven by the push for more flexible, scalable, and data-centric approaches to water management. The rise of the as-a-Service business model (e.g. Software-as-a-Service, Data-as-a-Service, and Network-as-a-Service) approach is key to the acceleration of cloud adoption. This trend will benefit smaller utilities with limited technical resources, as they can easily rely on third-party vendors and service providers to handle the day-to-day operations and maintenance of cloud-based systems.

As digital systems become more integral to utility operations, the sector faces growing risks from cyberattacks. Bluefield Research projects that cybersecurity spending in the water sector will grow at a 7.5% CAGR from 2024 to 2033. This increase reflects the growing need to safeguard critical systems that are vulnerable to threats, such as ransomware, phishing attacks, and operational disruptions.

These needs and challenges add up to significant opportunities for companies that are targeting and investing in digital water. From engineering companies to SCADA companies to software companies, there is ample opportunity to help utilities manage their digital transformation process—including both mature utilities furthering their journeys as well as smaller resource-strapped utilities that don’t have in-house capabilities.

“While the market has traditionally been dominated by large water industry technology incumbents, innovative startups have emerged to challenge their market dominance by offering equivalent solutions at more accessible price points. At the same time, technology firms, from adjacent sectors, such as AWS, Microsoft, and Oracle continue to seek opportunities to apply their digital expertise to the water sector,” says Ow.

About this Report

U.S. & Canada Digital Water Market Outlook: Key Drivers, Competitive Shifts, and Forecasts, 2024–2033

This Insight Report provides a forecast of utility spending on digital water across 36 technology segments by geography, technology segment, product type, water type, utility size, spend type, and software type to determine the size and growth outlook of the U.S. and Canada digital water market from 2024 to 2033. Bluefield provides a detailed view of the current landscape and future growth, along with insights into major market drivers and trends, the competitive environment, and detailed company profiles of 15 major digital water incumbents. The report (and accompanying data dashboard) is available for purchase and immediate download from Bluefield’s website. (or included with a Digital Water Corporate Subscription)

Source: Bluefield Research