Australia's US$17.4B Digital Water Forecast Highlights The Utility Opportunity Ahead

Australia’s water utilities stand at the global forefront of advanced water management, a position forged by the Millennium Drought (2001–2010) and sharpened by two decades of hard-won operational experience. The proliferation of digital technologies—smart meters, network monitoring, and AI-enabled analytics—has made Australia an epicenter of digital water innovation, representing a US$17.4B market opportunity through 2036.

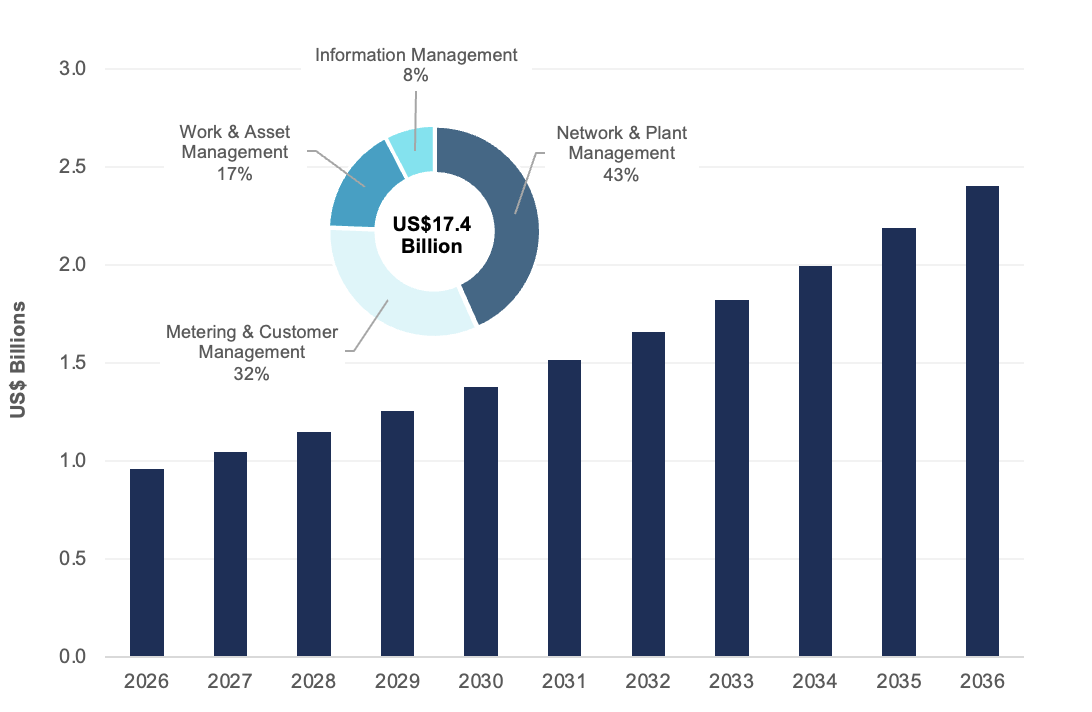

A new report from Bluefield Research, Australia Digital Water Landscape: Utility Strategies, Competitor Dynamics, and Growth Forecasts, 2026–2036, projects that total expenditures on digital solutions will grow from US$958.6 million in 2026 to US$2.4B in 2036. At a 9.6% compound annual growth rate (CAGR), the country’s digital water expenditures are set to more than double over the next decade.

“Decades of infrastructure investment have established Network & Plant Management as the market’s largest segment at 43%, but the momentum is shifting,” says Leigh Ramsey, a senior analyst at Bluefield Research. “Metering & Customer Management, at 32% and accelerating, reflects where utilities are placing their bets, with digital tools that directly drive water efficiency and customer engagement.”

Exhibit: Australia Digital Water Forecast, 2026–2036

A Market Centered on Urban Concentration

The landscape for digital vendors and service providers is structurally unique, headlined by 16 large urban utilities that serve 82% of the population. Three utilities—Sydney, Melbourne, and Brisbane—account for 40% of total digital market value. These major urban utilities, equipped with dedicated innovation teams and significant capital programs, are setting the technology and procurement benchmarks the rest of the country will follow.

The clearest expression of that momentum is smart metering. Sydney Water and South East Water have committed to full-scale rollouts covering nearly 30% of the national population, and 15 of the top 20 utilities have active pilots underway representing a further 46% of Australians. Static meter deployments are forecast at a 15.6% CAGR, with customer engagement software growing even faster at 23.7% as utilities use real-time data to manage demand and build customer trust. Foundational solutions—Supervisory Control and Data Acquisition (SCADA), Geographic Information System (GIS), and network monitoring—remain the backbone of utility spend, but larger utilities are now layering artificial intelligence (AI)-enabled analytics on top, moving from reactive infrastructure management to predictive, data-driven decision making.

“Non-revenue water at major urban utilities has risen 25% in five years, and with capital expenditures (CAPEX) up 83% over the past decade, utilities are under intense pressure to demonstrate that digital investment delivers measurable efficiency gains,” Ramsey notes.

Growth Intensifies Competition

Australia’s digital water landscape is being contested on two fronts: large urban utilities that attract a fragmented mix of multinationals and local specialists, and smaller rural utilities that are served predominantly by local vendors differentiated through end-to-end service delivery, deep market knowledge, and longstanding relationships. At the urban level, global players such as Siemens, Xylem, and Veolia compete directly with locally founded specialists like Taggle and Detection Services, which leverage multi-year contracts and integrated service models to hold their ground against larger competitors. This competition is intensifying as smart metering shifts from pilot to full-scale deployment, lowering barriers to entry and opening the door to new entrants like Sagemcom and Huizhong.

Cutting across both fronts is the outsized influence of engineering firms, deeply embedded in utility capital programs and playing a decisive role in hardware and software selection. GHD, WSP, Aurecon, Jacobs, Stantec, and Mott MacDonald have secured five-to-ten-year capital delivery partnerships with Australia’s largest utilities, making them de facto gatekeepers for technology procurement. For vendors, the path to winning in Australia runs as much through these engineering partnerships as it does through the utilities themselves.

“While relatively small in total volume compared to larger global markets like the U.S. and select EU countries, the underlying drivers—climate urgency, utility demand, and a demonstrated openness to innovation—make Australia one of the most compelling digital water landscapes in the world,” Ramsey observes.

About Bluefield Research

Bluefield Research supports strategic decision–makers with actionable water market intelligence and data in the global industrial and municipal sectors. With expertise spanning infrastructure, policy, and technology, Bluefield helps companies understand where the market is going—and why.

The Insight Report, Australia Digital Water Landscape: Utility Strategies, Competitor Dynamics, and Growth Forecasts, 2026–2036, provides a comprehensive analysis of Australia’s digital water landscape, including drivers and trends, competitive dynamics, detailed profiles of more than 20 major digital water incumbents, and profiles of key utilities. The full report is available for purchase and can be downloaded immediately from Bluefield’s website.

Source: Bluefield Research